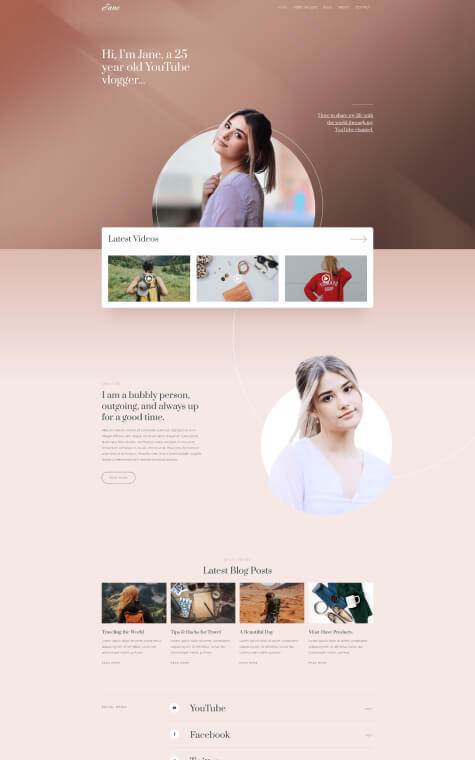

{ jane blogger }

//...website design & lorem ipsum dolor sit amet, consectetur adipiscing elit; ut elit tellus, luctus nec ullamcorper mattis;

{ patisserie }

//...front-end development & lorem ipsum dolor sit amet, consectetur adipiscing elit;

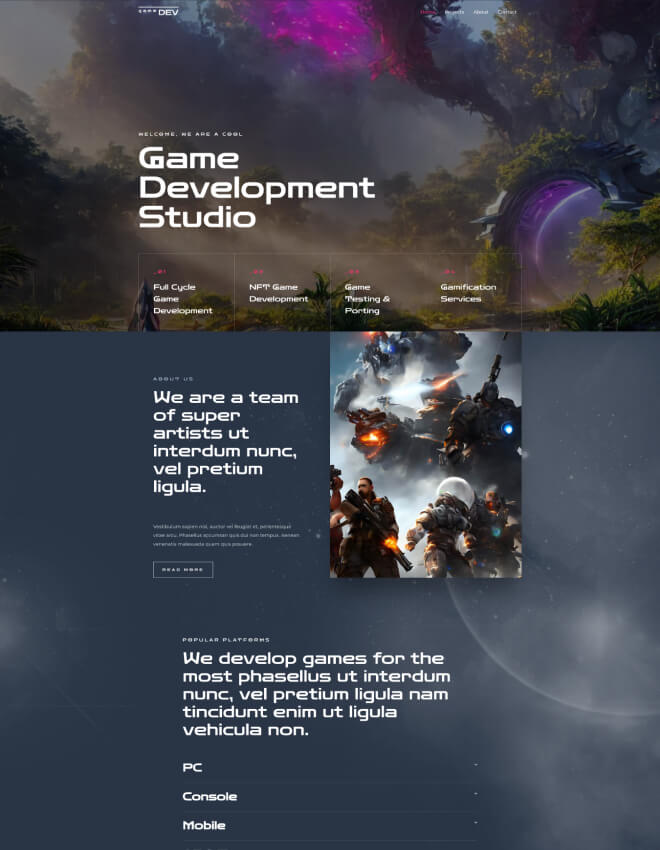

{ game_studio }

//...website design & lorem ipsum dolor sit amet, consectetur adipiscing elit; ut elit tellus, luctus nec ullamcorper mattis;

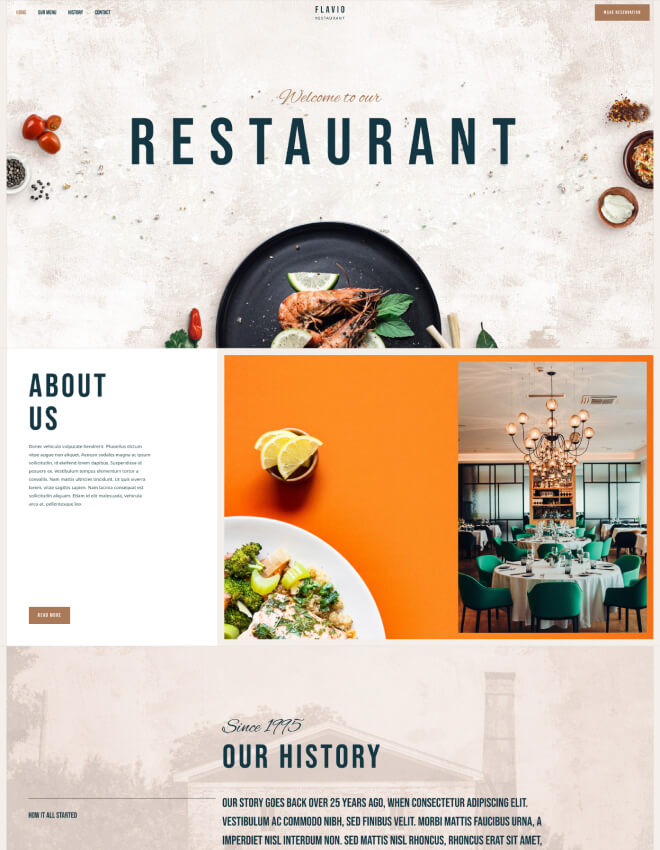

{ restaurant }

//...website design & lorem ipsum dolor sit amet, consectetur adipiscing elit;

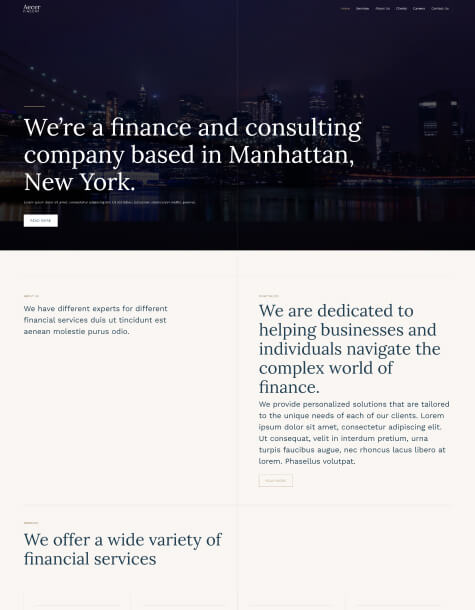

{ aecer fincorp }

//...website design & lorem ipsum dolor sit amet, consectetur adipiscing elit;

{ blockchain }

//...website design & lorem ipsum dolor sit amet, consectetur adipiscing elit; ut elit tellus, luctus nec ullamcorper mattis;